In many ways, it’s an honour when someone asks you to guarantee their loan. It’s a sign of their trust in you - an indication of the strength of the relationship. And it can feel fantastic to give someone a helping hand.

Whether you’re helping a family member, friend or business partner, you deserve to take a moment to acknowledge that this invitation is, in its own way, a sign of your own success. And perhaps you can also remember the people who helped you achieve your own wealth creation and wealth protection goals.

But…

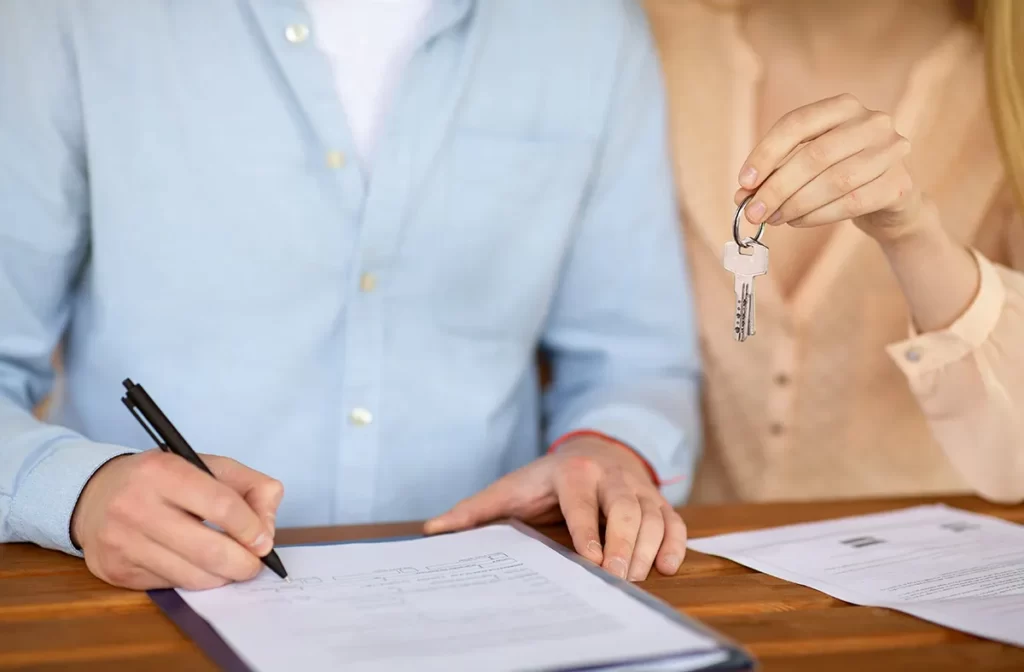

Going guarantor on a loan is also a big responsibility.

It might feel like it’s only writing your name on a piece of paper. But that signature carries a lot of weight:

If you guarantee a loan for a family member or friend, you're known as the guarantor. You are responsible for paying back the entire loan if the borrower can't.

Source: Money Smart

Is it worth the risk to enter into this serious, legally binding contract? Ultimately, that’s a question only you can answer. And the best way to do that is, as always, to talk to your trusted financial advisor.

In this article, we’ll outline a few considerations to take with you to that meeting, including:

- The risks of going guarantor on a loan

- Types of guarantee agreements

- What happens in the worst-case scenario.

What is a loan guarantor?

In 2023, many young - or even mid-career - people won’t get into the housing market without help from the bank of mum and dad. Similarly, securing a mortgage can depend on having a solid guarantor in your corner - and this help usually comes from a legal guardian.

However, any kind of personal loan can have a guarantor arrangement to support it. It’s important to remember that conditions vary by lender and loan product type.

What are the risks of going guarantor on a loan?

The ultimate risk of going guarantor is that you could end up having to pay back the entire loan out of your own pocket. That could mean:

- setting aside part of your salary

- dipping into your savings

- selling investments

- consolidating your own loans.

The lender could repossess your assets (like your home or your car) if they were used as security for the loan.

The worst-case scenario? Bankruptcy.

Other risks:

- If you’re already a guarantor on a loan, even if it is being repaid, a lender may decide not to extend credit to you.

- If things go wrong and the borrower can’t pay back the loan, this will affect your own credit rating.

- Love and money don’t always mix. Do consider how this could affect your relationship.

Your financial advisor can help mitigate those risks

Despite the risks, there are ways to safely go guarantor on a loan and enjoy the warm, fuzzy feelings outlined above.

1 - Assess the risk

Your financial advisor can help you ask the right questions and put the answers into context, based on the borrower’s financial state of affairs, including personal details such as:

- Profession and income

- Credit rating and viability

- Other financial obligations.

2 - Get the right guarantor agreement

The two types of guarantor agreements have different risk profiles:

- A limited guarantor agreement has a cap on the amount and duration of the loan

- An unlimited guarantee extends your liability to the full amount due, including the principal and interests, and without a definite timespan.

A limited agreement is the safer option. For an unlimited agreement, you’ll need to consider mitigation strategies such as guarantor insurance to cover or lessen your financial burden in the event that the borrower defaults on the loan.

3 - Check in

There’s no need to ‘set and forget’ your loan guarantor arrangement.

It’s completely reasonable (and recommended) to ask for updates on the balance, payments, due dates and any relevant changes.

Once the payments are 90 days in arrears, you’re in trouble: that’s when the lender is most likely to issue the borrower with a notice of default (source: Reserve Bank of Australia).

A proactive financial advisor could take all those tasks off your to-do list.

If things do go badly… what are your options? Again… you’ll want a financial advisor in your corner if things do go wrong. Your options include:

- Renegotiating a payment plan.

- In rare circumstances (e.g. if the creditor violated a term of the arrangement) engaging a legal defence.

Are there other ways to help?

If in the end you decide to decline the invitation to go guarantor on a loan, there are other ways you can help (while also protecting your own wealth).

- It might be more comfortable for you to make a financial gift to go towards the initial deposit.

- If the loan is for a startup or business expansion, perhaps it’s a great opportunity for you to invest - or volunteer as a mentor.

- Offer your services as a business advisor.

- If it’s a matter of getting your kids into the housing market, but you’re not ready to guarantee their loan, help them to save. Can you offer them a period of living back at home, so they can save on rent?

One small note

It’s never okay to pressure someone into a financial commitment of any kind. Unfortunately, financial abuse can happen to anyone. If an invitation to go guarantor feels more like an obligation, it’s especially important to talk to your trusted advisor to make a well-informed plan to protect yourself and your relationships, as well as your wealth.

Is going guarantor a good idea for YOU?

Even with these safety tips in mind, it’s still critical that you consult an independent professional before committing to any guarantor agreement.

This will give you a unique perspective on the guarantor request that’s separate from the lending institution and the borrower, enabling you to make a decision that works best for your financial goals. You’ll want to ask the questions that are most important to your unique financial situation, like “How will becoming a

guarantor affect my goal to retire in the next five years?”

With 20+ years of experience, Anthony Poole of Poole Advisory is well placed to give personalised wealth protection advice.

“Poole identified ways we can build our wealth that we never thought of. We’re now planning to fully retire in 12 months while maintaining our comfortable lifestyle.”

Veronica M, Poole Advisory Client

Contact Poole Advisory today or book a meeting to start your financial planning journey.

Sorting your finances with Poole Advisory

Compliance Disclaimer:

This information contains general advice only, that is, advice which does not take into account your needs, objectives, or financial situation. You need to consider the appropriateness of that general advice in light of your personal circumstances before acting on the advice. You should obtain and consider the Product Disclosure Statement for any product discussed before making a decision to acquire that product. You should obtain financial or credit advice that addresses your specific needs and situation before making investment or borrowing decisions. Taxation information is based on our interpretation of the relevant laws as at 1 July 2018. While every care has been taken in the preparation of this information, Prosperitas Partners Pty Ltd does not guarantee the accuracy or completeness of the information. The case studies are hypothetical, for illustration purposes only and are not based on actual returns

Poole Advisory Pty Ltd ABN 15 642 040 604 is a Corporate Authorised Representative (No. 001282603) of Prosperitas Partners Pty Ltd ABN 30 662 654 453 AFSL 544 917